MANFAATken MOMENTUM PENUNDAAN KENAEKAN THE FED FUND RATE K 2016 dengan KEBIJAKSANAAN BI RATE DI BAWAH 7%

0..

LIMA - Dana Moneter Internasional (IMF) memberikan peringatan kepada para gubernur bank sentral, termasuk Federal Reserve AS (Fed) bahwa ekonomi dunia dalam risiko bahaya lain, kecuali mereka terus mendukung pertumbuhan dengan suku bunga rendah.

Lembaga pemberi pinjaman dunia berbasis di Washington ini menyebutkan, dalam komunike akhir bahwa ketidakpastian dan volatilitas pasar keuangan telah meningkat, dan prospek pertumbuhan jangka menengah melemah.

"Di banyak negara maju, risiko utama tetap penurunan pertumbuhan yang rendah. Dan ini perlu didukung dengan kebijakan moneter lanjutan yang akomodatif, dan stabilitas keuangan membaik," ujar Managing Director IMF Christine Lagarde dalam pertemuan akhir para Gubernur Bank Sentral G-30 di Lima, Peru, seperti dilansir dari The Guardian, Minggu (11/10/2015).

Dia mengatakan ada risiko "spillovers" ke pasar keuangan stabil dari bank sentral AS dan Inggris bila meningkatkan biaya kredit. IMF juga mendesak Jepang dan Zona Euro untuk mempertahankan rencana mereka merangsang ekonomi yang sakit dengan peningkatan pelonggaran kuantitatif (quantitative easing).

Tapi, Lagarde mendesak para pembuat kebijakan di Jepang dan Zona Euro untuk meningkatkan ekonomi mereka dengan ekspansi pinjaman bank dan bisnis melalui pelonggaran kuantitatif tambahan.

New York -Pasar saham Wall Street berakhir negatif menyusul turunnya harga minyak dunia hingga ke bawah US$ 40 per barel. Komentar Gubernur The Federal (The Fed) Janet Yellen makin menjurus ke adanya kenaikan suku bunga bulan ini.

Aksi penembakan di selatan California juga membuat investor melepas saham jelang penutupan perdagangan. Indeks sektor energi jatuh 3,1% dipimpin oleh saham-saham perusahaan migas.

Petinggi The Fed lagi-lagi memberi isyarat ada kemungkinan kenaikan suku bunga di bulan ini karena ekonomi AS sudah mulai membaik. Pertemuan The Fed selanjutnya akan digelar pada 15-16 Desember.

"Saya sedikit kaget melihat Yellen begitu yakin (suku bunga bisa naik). Pernyataan ini ia lontarkan hanya dua hari sebelum pengumuman tenaga kerja dan sepekan sebelum pertemuan The Fed," kata Michael O’Rourke, kepala investasi pasar dari JonesTrading di Greenwich, Connecticut, seperti dikutip Reuters, Rabu (3/12/2015).

Pada penutupan perdagangan Rabu waktu setempat, Indeks Dow Jones melemah 158,67 poin (0,89%) ke level 17.729,68, Indeks S&P 500 anjlok 23,12 poin (1,1%) ke level 2.079,51 dan Indeks Komposit Nasdaq berkurang 33,08 poin (0,64%) ke level 5.123,22.

(ang/ang)

Hong Kong, Oct 9, 2015 (AFP) Shares in Hong Kong and mainland China rallied in line with other global markets Friday as traders cheered minutes from the Federal Reserve's latest meeting suggesting it could put back an interest rate hike to next year.

The benchmark Hang Seng Index in Hong Kong ended up 0.46 percent, or 103.89 points, to 22,458.80.

In Shanghai the composite index rose 1.27 percent, or 39.79 points, to 3,183.15, while the Shenzhen Composite Index, which tracks stocks on China's second exchange, gained 1.47 percent, or 26.24 points, to 1,811.63.

0.A.

WASHINGTON, KOMPAS.com - Bank Sentral AS atau

The Federal Reserve (The Fed) akhirnya membuat keputusan dengan

mempertahankan suku bunga acuannya 0 persen pada Kamis (17/9/2015).

Keputusan itu diambil di tengah stagnasi pertumbuhan ekonomi di AS dan

pelambatan ekonomi dunia.

Meski begitu, Komite Pasar Terbuka Federal (The Federal Open Market Committee/FOMC) sempat merencanakan menaikkan suku bunga acuannya pada akhir tahun ini.

"Kondisi

ekonomi dan keuangan dunia saat ini mungkin menahan aktivitas ekonomi,

ini yang membuat tekanan terhadap inflasi," kata The Fed.

Dijelaskan,

gejolak perekonomian dunia saat ini lebih dikarenakan melemahnya

ekonomi China. Disebutkan The Fed, pihaknya terus memantau setiap

perkembangan di China, terlebih jika nantinya perekomian AS terkena

imbas terbesar.

The Fed menggelar rapat selama dua hari ini

membahas kebijakan apakah akan mengambil keputusan dengan menaikkan suku

bunganya sejak sembilan tahun terakhir, sekaligus mewaspadai krisis

seperti yang terjadi di tahun 2008.

Diingatkan The Fed, kondisi

ekonomi di AS saat ini berada dalam posisi moderat, dengan pengeluaran

rumah tangga dan investasi yang meningkat, bersama dengan peningkatan

pembangunan rumah.

Salah satu kunci dari kebijakan yang diambil

The Fed adalah kekuatan dari pasar tenaga kerja. Dikatakan, perkembangan

pasar tenaga kerja sudah meningkat sejak pertemuan Juli lalu. Meski

begitu, tingkat inflasi menjadi rujukan paling utama dari The Fed

The

Fed menekankan, pertumbuhan ekonomi AS akan meningkat 2,1 persen tahun

ini namun di tahun 2016 diproyeksikan melambat 2,3 persen dari 2,5

persen yang diperkirakan.

The Fed juga menurunkan proyeksi

inflasinya selama dua tahun mendatang, diperkirakan 1,7 persen pada

tahun depan dan 1,9 persen pada 2017. Proyeksi ini di bawah perkiraan

2,0 persen sebelumnya

Keputusan The Fed ini tidaklah mengejutkan

pasar, perdagangan di Wall Street pun tetap moderat, indeks S&P naik

0,33 persen di penutupan perdagangan. Sementara, dollar AS melemah 1,0

persen dengan nilai tukar 1,1395 atas Euro.

bloomberg: U.S. stocks ended lower after

swinging between gains and losses, as the Federal Reserve’s decision to

keep interest rates near zero percent raised questions about the

strength of the global economy.

The Fed kept its policy interest

rate unchanged, showing reluctance to end an era of record monetary

stimulus in a time of market turmoil, rising international risks and

slow inflation at home. Stocks erased an advance after Chair Janet

Yellen indicated that global developments overshadowed signs of strength

in America.

Stocks fluctuated after Fed

“It’s a bit of a tussle,” said

Carin Pai, director of equity strategy at Fiduciary Trust Company

International in New York. Her firm manages $17.4 billion. “If they

don’t raise rates and continue to hold off on raising rates, what does

that say about the economy? That it’s not strong enough to withstand an

interest rate increase. That’s what the market is grappling with right

now.”

The Standard &

Poor’s 500 Index fell 0.3 percent to 1,990.20 at 4 p.m. in New York,

reversing a gain of as much as 1.3 percent. The Dow Jones Industrial

Average slipped 65.21 points, or 0.4 percent, to 16,674.74. Stocks most

sensitive to interest rates had the largest moves, with utilities and

real-estate companies advancing at least 0.9 percent while banks lost

2.4 percent.

The decision to stand pat on rates keeps a pillar of

the bull market in place, as record-low borrowing costs have helped

propel stocks higher by nearly 200 percent in the past 6 1/2 years.

It

also amplifies uncertainty about the strength of the American economy

at a time financial markets have been roiled by concern that a slowdown

in China will spread. The S&P 500 had fallen 3.3 percent this year

after three years of double-digit gains.

At 5.1 percent, U.S.

unemployment is the lowest in seven years and housing sales are

rebounding, giving ample evidence that the economy is finding firmer

footing. But inflation has remained below the objective of Fed policy

makers amid a 50 percent plunge in energy costs over the past 12 months and a rising dollar.

Economic Driver

“Yellen wants to make sure that the U.S. remains the driver of global economic health,” said

Dan Veru, who helps oversee $5 billion as chief investment officer at

Fort Lee, New Jersey-based Palisade Capital Management. “The U.S. has to

be the engine for pulling the globe out of slow growth.”

The

argument against tightening got a boost from concern that, with central

banks from Asia to Europe considering adding stimulus, any Fed move

would have fueled a rally in the greenback. A stronger dollar may crimp profits at exporters at a time when analysts forecast earnings at S&P 500 companies will fall in the final two quarters of 2015.

“Now

that this is behind us, people are going to start focusing more on the

problems that caused the correction in August, which is weakness in

China and other emerging markets and a rough time on the earnings

front,” said Matt Maley, an equity strategist at Miller Tabak & Co LLC in New York.

The decision to keep rates near zero wasn’t a surprise given the weakness on U.S. equity markets. In four

tightenings since 1990, including the tapering of bond purchases

announced in 2013, the S&P 500 had posted positive returns over the

prior three and six month periods, and was within 3 percent of the

gauge’s 52-week high, according to a Bank of America Corp. report.

By

comparison, the benchmark index was down 4.8 percent over the last

three months through yesterday and 6.4 percent below its high of

2,130.82 reached in May. The S&P 500 has alternated between gains

and losses for the past nine weeks, a streak of indecision that’s

happened only three times in 20 years, according to data compiled by

Bloomberg.

High Volume

The rate decision came in a market

where the role of computers has grown drastically since the last time

the Fed raised rates. With high-frequency firms accounting for about

half of trading in the U.S., daily volume has tripled since the early

2000s and now regularly tops 6 billion shares. Trading on U.S. exchanges

today was 8 billion, 12 percent above the three-month average.

The

market has whipsawed since China’s shock devaluation of its currency on

Aug. 11, a move that sent the S&P 500 to its first 10 percent

decline since 2011. The Fed has never started tightening within a month

of a correction.

Market anxiety has been elevated amid concern

that higher U.S. rates could rattle emerging markets and threaten global

growth. Price swings on the S&P 500 have widened to 1.5 percent a

day in the past month, compared with 0.6 percent this year through July.

The

Chicago Board Options Volatility Index endured its biggest weekly gain

on record in August, and has closed above 20 for 19 straight sessions,

the longest stretch since June 2012. The gauge fell 1 percent to 21.14 on Thursday.

Seven

out of 10 major groups in the S&P 500 advanced, led by gains in

utilities, consumer-discretionary and health-care shares.

Cablevision

Systems Corp. soared 14 percent to the highest level since 2001 after

Altice NV agreed to buy the cable TV and Internet service provider in a

$17.7 billion deal.

Airlines rallied after Barclays said the

latest leg lower for oil is a “positive ongoing catalyst” for the

industry. United Continental Holdings Inc. jumped 6.2 percent, American

Airlines Group Inc. gained 2.2 percent and Spirit Airlines Inc. rose 6.7

percent, the most since January.

Oracle Corp. declined 4 percent

after reporting first-quarter revenue that fell short of analysts’

projections. Verizon Communications Inc. slid 2.1 percent after it said

2016 earnings could plateau at 2015 levels as the company deals with

business model changes and a sale of some wireline assets.

Rite

Aid Corp. lost 11 percent after the drugstore chain cut its forecast for

profit and revenue on expectations for slower growth in stores that

have been open at least a year.

Peabody Energy Corp. tumbled 11

percent as shareholders authorized a reverse stock split designed to

keep the company listed on the New York Stock Exchange.

1a.tambahan:

Jakarta detik -Survei terbaru oleh Business Rountable dan PwC menyebutkan, sebagian besar dari para pebisnis atau CEO di Amerika Serikat (AS) meyakini bahwa di 2016 perekonomian AS masih belum membaik.

Melihat hal itu, kebanyakan dari mereka tidak akan agresif memasang target dalam menjalankan bisnisnya. Itu bukan berita baik bagi perekonomian.

Ketika para pemimpin bisnis optimistis tentang masa depan, mereka akan lebih banyak berinvestasi dan mempekerjakan lebih banyak orang dan mengembangkan produk-produk baru. Hal ini akan mendorong pertumbuhan ekonomi ke depan.

Tapi sekarang kondisinya tidak demikian. Diperkirakan untuk investasi bisnis 2016 masih akan redup. Ini adalah kondisi terburuk sejak 2009 ketika AS masih dalam resesi besar.

"Terjadi penurunan tajam dalam investasi, ini mengkhawatirkan," kata Randall Stephenson, CEO AT&T (T,Tech30) dan Ketua Business Rountable seperti dilansir CNN.com, Sabtu (5/12/2015).

Stephenson menyalahkan perlambatan yang terjadi pada ekonomi global. Para pebisnis ini kecewa terhadap para pengambil kebijakan yang tidak melakukan reformasi pajak perusahaan.

"Jika kita ingin melihat ekonomi AS bertumbuh, Washington perlu mengadopsi pendekatan yang lebih cerdas untuk regulasi," ujarnya.

Menurut Stephenson, pajak yang diterapkan saat ini tidak kompetitif bagi dunia usaha sehingga mereka cenderung 'melarikan diri' dari AS untuk mencari pajak yang lebih rendah seperti di Eropa atau di tempat lain.

Misalnya, perusahaan besar yang bergerak di bidang obat-obatan asal AS Pfizer (PFE) baru saja mengumumkan kesepakatan untuk membeli perusahaan raksasa asal Irlandia yang berbasis di Allergan.

Mereka berencana untuk memindahkan kantor pusat mereka di luar negeri dan mencari pajak yang lebih rendah.

Perlambatan ekonomi global ini merupakan masalah besar.

Pesimisme juga terlihat dari para eksekutif. Dalam survei terbaru disebutkan bahwa lebih dari 200 eksekutif dari perusahaan swasta meyakini bahwa ekonomi global saat ini tengah terpuruk.

Devaluasi yuan oleh China pada bulan Agustus lalu memicu pasar saham global jatuh, ini membebani para pebisnis di AS.

Hanya seperempat dari para eksekutif yang disurvei oleh PwC berencana untuk menanamkan investasi baru, angka ini turun 36% dibanding kuartal sebelumnya.

Dan hanya lebih dari setengah dari perusahaan yang disurvei, berencana untuk melakukan perekrutan karyawan, ini juga merupakan penurunan dari tahun sebelumnya.

Tapi, kondisi demikian tidak seperti krisis di 2007 atau 2008. Tidak ada situasi yang mengerikan seperti saat itu. Business Rountable memprediksi ekonomi AS akan tumbuh 2,4% tahun depan, hampir sama dengan tahun ini alias stagnan.

(drk/rrd)

the guardian: Federal Reserve officials were almost ready to raise interest rates in September but held off because of China’s economic slowdown and its potential to derail US growth and inflation.

Minutes of the 16-17 September discussions showed the central bank believed the time for the first Fed rate increase in nine years “might be near”.

But policymakers decided that it would be “prudent to wait” for evidence that the economy had not deteriorated and that inflation would gradually move back toward the Fed’s 2% annual target. Some members also expressed concerns that a premature rate hike could harm the central bank’s credibility.

The September meeting had been preceded by weeks of speculation over whether rates would be increased. The Fed decided against a rate hike, although various officials have indicated it was a close call.

Fed chair Janet Yellen told reporters at a news conference following the meeting that a rate hike was still likely this year, a prediction she repeated two weeks ago during a speech in Massachusetts.

But since then, the government has released economic data that could give Fed official further pause.

Employers added just 142,000 jobs in September, and officials lowered their estimate of job gains in July and August by a combined 59,000. That left monthly job growth at a mediocre 167,000 in the July-September period, down from 231,000 in the April-June period.

Many economists believe the weak job report has eliminated the possibility of a rate hike at the next meeting in October. Some believe the Fed could end up waiting until next year to begin raising rates.

The Fed’s two final meetings of this year will occur on 27-28 October and 15-16 December.

“I believe the jobs report makes an October rate hike out of the question, but if we have some strong employment reports before the December meeting, then a case could still be made from a December rate increase,” said Sung Won Sohn, an economics professor at the Martin Smith School of Business at California State University.

The Fed has kept its benchmark rate at a record low near zero since December 2008. It has not raised rates since June 2006.

Oleh Ryan Filbert @RyanFilbert

KOMPAS.com - Pertanyaan ini sempat ditanyakan kepada saya beberapa bulan terakhir ini. Apalagi hampir setiap bulan selalu ada berita di mana-mana yang mengatakan Federal Reserve (The Fed) tidak jadi menaikkan suku bunga. Lah, lantas sebenarnya ada apa sampai-sampai kebijakan ini juga ditunggu oleh pelaku pasar di Indonesia bahkan hingga di seluruh dunia?

Agar kita memahami kondisi The Fed di Amerika Serikat ini, setidaknya kita perlu mengetahui bahwa beberapa tahun yang lalu, terjadilah sebuah peristiwa bersejarah mengenai krisis kredit perumahan di AS yang dikenal dengan "Krisis Subprime Mortgage" tepatnya pada tahun 2008.

Berbeda dengan negara kita tercinta Republik Indonesia, negara-negara di Amerika dan juga Eropa terjadi sebuah perlambatan ekonomi yang ditandai dengan minimnya pertumbuhan inflasi di negara-negara tersebut. Untuk mengatasi krisis, maka pemerintah Amerika melakukan sebuah kebijakan ‘uang murah’ yang dikenal dengan Quantitative Easing (QE).

Nah, QE ini adalah sebuah strategi membanjiri pasar dengan uang berbunga murah sampai dengan gratis. Jadi dalam bayangan sederhananya, negara memanggil bank-bank yang ada lalu bank tersebut diberikan sejumlah dana untuk disalurkan.

Apa tujuannya? Agar dengan bunga yang murah itulah para rakyatnya dapat menggunakan uang lebih konsumtif sehingga akan berdampak pada naiknya tingkat inflasi di negara tersebut.

Ya, inflasi itu kenaikan harga dan harga naik karena permintaan terhadap barang meningkat, teori ekonomi sederhana saja.

Masalah negara maju adalah masyarakatnya memang tidak terlalu gemar konsumsi, tidak seperti Indonesia yang masih berkembang. Alhasil, uang yang diberikan dengan bunga murah, bahkan gratis, ini justru malah digunakan untuk berinvestasi. Bursa AS telah pulih dan mendobrak rekor tertingginya kembali di tahun 2013.

Pulihnya bursa bukan diakibatkan karena perekonomian membaik, melainkan efek uang berbunga murah masuk ke pasar-pasar investasi di bursa. Nah, uang hasil ‘pinjaman’ oleh AS dari QE itu, yang seharusnya bertujuan meningkatkan inflasi AS, justru mengalir ke banyak negara lain, termasuk ke Indonesia, baik masuk ke bursa atau pasar modal maupun dalam bentuk lainnya.

Sadar karena jurus uang murahnya tidak memperbaiki kondisi perekonomian, maka si uang murah ini ditarik kembali, yang dikenal sebagai istilah ‘tapering’. Dan salah satu jurus dari negara dan bank sentralnya untuk mengendalikan uang beredar adalah dengan melakukan kebijakan menaikkan suku bunga.

Sebagai pengendali yang memberikan keputusan atas kebijakan moneter AS, The Fed sepanjang tahun 2015 ingin melakukan sebuah kebijakan ‘menarik uang murah’ dengan menaikkan suku bunga.

Di sinilah letak kekhawatiran para pelaku pasar di dunia, karena uang-uang murah menghuni pasar modal, yang bila dananya ditarik dalam satu momen akan terjadi penurunan.

Oleh karena itulah kebijakan The Fed menjadi sebuah penantian bagi pelaku pasar karena dikhawatirkan dampaknya akan membuat pasar finansial mengalami penurunan, termasuk di Indonesia.

Harga saham yang kebanjiran uang murah tentunya akan meroket dan berubah dari harga wajar menjadi harga yang tidak wajar ibarat membeli nasi goreng di gerobak dengan membeli nasi goreng di hotel, sama-sama nasi goreng tapi harganya berbeda.

Pada saat ini menjadi sebuah kekhawatiran akan jatuhnya saham-saham berharga tidak wajar kembali ke harga semula akibat ketidaksesuaian dengan kinerja perusahaan sebenarnya.

Meskipun The Fed akan mempertahankan ataupun menaikkan suku bunganya, seorang investor perlu melihat nilai perusahaan dibandingkan berfokus pada harga saham, hanya seorang pedagang yang sangat peduli dengan harga.

Salam investasi untuk Indonesia.

bloomberg:

Federal Reserve policy divisions were exposed Tuesday as Governor

Daniel Tarullo argued interest rates should stay on hold while documents

showed most regional Fed directors sought higher borrowing costs,

challenging Chair Janet Yellen to maintain consensus.

Tarullo told CNBC that he doesn’t currently favor raising interest rates in 2015. That lines him up with fellow Governor

Lael Brainard, who made the case on Monday for patience, and diverges

from the majority of Federal Open Market Committee members including

Yellen. She said on Sept. 24 that she expected the first increase since

2006 to be warranted by year-end. Yellen hasn’t since spoken publicly on

policy.

The dovish remarks from two of the five members of the

Fed Board in Washington are an unusually sharp contradiction of the

Fed’s leadership and set the stage for a robust debate at the central

bank’s two remaining policy-setting meetings this year.

Vice Chair

Stanley Fischer said Sunday a move was still needed this year so long as

the economy grows as expected, and New York Fed President William C. Dudley has also placed himself in the 2015 liftoff camp. The Fed meets on Oct. 27-28 and Dec. 15-16.

Eight out of Twelve

Minutes

from the central banks’ discount-rate meetings released Tuesday showed

that eight of 12 regional Fed bank boards voted in September to raise

the discount rate, or the rate charged to banks for direct loans from

the Fed. The Board in Washington declined to implement their request.

The split -- in which regional heads including St. Louis’s James Bullard and Richmond’s

Jeffrey Lacker are pushing Yellen to get going while board members

including Brainard and Tarullo urge caution -- hinges on how officials

read the economy.

Some look toward falling unemployment and

sustained consumer spending and see an outlook in which U.S. growth

closes in on the economy’s longer-run potential. Others see

still-subdued inflation and a lack of wage growth and argue that the

risks to raising rates outweigh the benefits.

“Right

now, my expectation is, given where I think the economy would go, I

wouldn’t expect it would be appropriate to raise rates,” Tarullo said in

the CNBC interview. “I want to hasten to add that that is an outlook

that changes based on developments in the economy.”

Chinese Uncertainty

Fed

officials last month opted to delay a rate rise to wait for more

information about how slowing growth in China impacts the U.S. outlook

for inflation and growth. Economic projections prepared for the meeting

show that 13 of 17 of the central bankers saw a rate rise as appropriate

this year.

Tarullo and Brainard’s comments suggested to economists they’ve joined Chicago Fed chief Charles Evans and Minneapolis’s Narayana Kocherlakota in refraining from seeking a 2015 rate rise.

“Even

with Yellen and Fischer recently identifying their ‘dots’ as among

those that foresee liftoff before year-end, the impression left is one

of a Board even more dovish than usual set against a group of Reserve

Bank presidents that are perhaps more hawkish than previously thought,”

Michael Feroli, chief U.S. economist at JPMorgan Chase & Co. in New

York, wrote in a note to clients. “We still believe the Yellen-Fischer

leadership can pull the committee together for a December liftoff.”

The

eight regional Fed bank boards last month pushed to boost the rate for

direct loans from the Fed to 1 percent from 0.75 percent, with St.

Louis, Atlanta and San Francisco’s boards all adding their support for

an increase, the meeting minutes showed.

Regional boards are

typically aligned with the views of their presidents, all of whom take

part in meetings of the policy-setting FOMC, said Carl Tannenbaum, chief

economist at Northern Trust Corp. in Chicago and a former Fed

economist. While the discount rate “is not the federal funds rate,” the

Fed’s primary policy tool, the votes “reflect feelings about whether

credit is too tight or too easy,” he said.

Tarullo highlighted

reasons for caution that center on uncertainties in his economic

outlook. The U.S. is “currently in a global disinflationary

environment,” the natural rate of unemployment may have fallen, and past

relationships between inflation and joblessness don’t seem to be

operating effectively, he said Tuesday.

“My own perspective is

that one should watch to see some tangible evidence that allows one to

make, to develop that reasonable confidence that inflation will return

to target,” Tarullo said on CNBC.

marketwatch: Former Fed Chairman Ben Bernanke said Monday that he was not sure the economy could handle four quarter-point rate hikes.

Some economists and Fed officials argue that the U.S. central bank should hike rates now to anticipate inflation.

That

argument assumes the Fed can raise rates 100 basis points and it

wouldn’t hurt anything, Bernanke said. ”That is not obvious, I don’t

think everybody would agree to that,” he added in an interview with CNBC.

Higher rates could “kill U.S. exports with a very strong dollar,” he said.

Bernanke

said the “mediocre” September employment report is a “negative” for the

U.S. central bank’s plan to begin hiking rates in 2015, as a

strengthening labor market was the key conditions for the Fed to be

confident inflation was moving higher.

Bernanke said he would not

second-guess Fed Chairwoman Janet Yellen, saying only that his

successor faced “tough” calls. He said the two do not speak on the

phone.

Bernanke said interest rates at zero was not “radically

easy” policy stance as some have suggested. He said he did not take

seriously arguments that zero rates was creating an uncertain

environment was holding down business investment

Bernanke defended his policies, noting the steady decline in the unemployment rate in recent years.

He

said that the slower overall pace of gross domestic product since the

Great Recession was due to a downturn in productivity and other issues

outside the purview of monetary policy.

“I am not saying things are great, I don’t mean to say that at all,” he said.,

Rather, to boost productivity and capital investment, the Fed “needs help from other policymakers,” he said.

Bernanke is doing a round of interviews tied to the Tuesday release of his memoir “The Courage to Act.”

He penned an op-ed in Monday’s Wall Street Journal, but distanced himself on CNBC from the headline: “How the Fed Saved the Economy.”

A better headline would have been the Fed can’t act alone, he said.

Bernanke said that the current zero level of interest rate is not an “emergency rate.”

The

former Fed chairman said the argument the U.S. central bank should

raise rates so it would have room to later cut them “doesn’t make any

sense.”

“If you raised rates too early and kill the economy, that doesn’t help you,” he said.

Bernanke said the Fed’s $4.5 trillion balance sheet was not “a big issue.”

When the time comes, the U.S. central bank will just let assets run off passively over time, he said.

In the interview, Bernanke defended his assertion in his book and an interview with USA Today that more bank executives should have gone to jail in the wake of the crisis.

“What

I was talking about is that we do know that…many big banks, the

Department of Justice assessed billions and billions of dollars against

the firms for bad behavior of various kinds,” he said.

“If there are bad actors, you should go after them” individually, he said.

Federal Reserve Chair

Janet Yellen said the U.S. central bank is on track to raise interest

rates this year, even as she acknowledged that economic “surprises”

could lead them to change that plan.

“Most FOMC participants,

including myself, currently anticipate that achieving these conditions

will likely entail an initial increase in the federal funds rate later

this year, followed by a gradual pace of tightening thereafter,” Yellen

said during a speech Thursday in Amherst, Massachusetts. “But if the

economy surprises us, our judgments about appropriate monetary policy

will change.”

Yellen, 69, spoke a week after the Federal Open Market Committee

left its benchmark federal funds target near zero, saying "recent global

economic and financial developments" might damp growth and inflation in

the U.S. Concerns over a slowdown in China following a surprise Aug. 11

devaluation of the yuan triggered turmoil in financial markets and

raised questions about the outlook for the global economy.

While “there wasn’t anything significant enough that changed in one week for her to give us a different take,” said

Tom Porcelli, chief U.S. economist at RBC Capital Markets LLC in New

York, Yellen “finally acknowledges that she, specifically, does believe

that a rate hike is appropriate this year.”

Porcelli expects a December increase, but thinks there’s a high hurdle to moving this year.

Slower demand from China, where growth is projected to drop below 7 percent this year, has helped push down commodity prices, sapping already low inflation in the U.S. The Fed’s preferred gauge of price pressures rose 0.3 percent in the year through July and has been under its 2 percent target since April 2008.

Fading Headwinds

“We

cannot be certain about the pace at which the headwinds still

restraining the domestic economy will continue to fade,” Yellen said in

her remarks Thursday. “Recent global economic and financial developments

highlight the risk that a slowdown in foreign growth might restrain

U.S. economic activity somewhat further.”

The

Fed has been forced to weigh headwinds against signs of continued

growth in the domestic economy. U.S. employers have added 1.7 million

jobs to payrolls this year, pushing unemployment down to 5.1 percent in August, its lowest in more than seven years.

“On

balance the economy is no longer far away from full employment,” Yellen

said in her speech. “In contrast, inflation has continued to run below

the Committee’s objective over the past several years, and over the past

12 months it has been essentially zero.”

Yellen highlighted that

inflation expectations have remained well-anchored, but said that the

central bank shouldn’t take it for granted that they will stay that way.

She said she thinks “temporary effects” of falling energy and

non-energy import prices are the driver behind the tepid inflation, and

expects price pressures to rebound barring further decline in crude oil

prices and further appreciation in the dollar.

1.a. tambahan A:

NEW YORK, KOMPAS.com - Goldman Sachs Group

Inc menyatakan, the Federal Reserve kemungkinan akan menunda kenaikan

suku bunga hingga 2016 atau bahkan mungkin lebih lama lagi.

"Perlambatan pada tingkat produksi dan tenaga kerja menjadi faktor

yang membenarkan penentu kebijakan untuk menahan suku bunga mendekati

nol lebih lama hingga 2016 atau bahkan melampaui," jelas Jan Hatzius,

chief economist Goldman Sachs di New York.

Pelaku pasar juga sudah memangkas taruhan mereka mengenai kemungkinan

kenaikan suku bunga the Fed pada tahun ini, kendati Pimpinan The Fed

Jannet Yellen dan William C Dudley menegaskan kenaikan suku bunga akan

dilakukan tahun ini.

Berdasarkan data yang dihimpun Bloomberg, kemungkinan bank

sentral AS menurunkan suku bunganya pada tahun ini sudah mengalami

penurunan menjadi 35,2 persen dari sebelumnya 60 persen pada akhir

Agustus. Kalkulasi ini berdasarkan asumsi bahwa rata-rata suku bunga the

Fed yang efektif 0,375 persen setelah dinaikkan, versus target range

suku bunga saat ini yaitu 0 persen-0,25 persen.

Sedangkan kemungkinan kenaikan suku bunga pada pertemuan 27-28

Oktober mengalami penurunan hingga 10 persen pasca dirilisnya data

tenaga kerja pada pekan lalu.

"Setelah dirilisnya data tenaga kerja AS, sangat sulit bagi bank

sentral untuk menaikkan suku bunga. Saya bertaruh tidak akan ada

kenaikan suku bunga untuk beberapa waktu ke depan," jelas Hideo

Shimomura, chief fund investor Mitsubishi UFJ Kokusai Asset Management.(Barratut Taqiyyah.)

WASHINGTON (MarketWatch) — The U.S. economy had been viewed as relative bright spot in a gloomy global landscape, but now the outlook at home has also grown darker.

Blame the September jobs report. The government on Friday said the economycreated a disappointing 142,000 new jobs last month, following an even meager increase in August. Wall Street had been expecting a gain of 200,000.

Since July, job creation has slowed to an average of 167,000 a month, well short of the average 260,000 increase in 2014.

Now many economists believe the Federal Reserve has no choice but to forgo an interest-rate increase in October — what would be the first in nearly a decade. And some think central bank will have to wait until 2016 to raise a benchmark rate that’s been near zero for seven years.

The future path of interest rates is only adding to the growing uncertainty that initially began in August, when reports of slower Chinese growth triggered stock-market selloffs around the world, including in the United States.

“October is out of the question,” said John Canally, chief economic strategist at LPL Financial, an investor-advisory firm.

Everyone knows a rate hike is coming, but the fuzzy timing means investors aren’t quite sure how to act. Buy bonds, sell stocks, stand pat, or what?

“The September jobs report continues to muddy the waters,” said Michael Arone, chief investment strategist of a U.S. unit of State Street Global Advisors. “I’ve been describing this territory as 'purgatory.’ ”

Investors won’t be getting out of purgatory anytime soon, either.

The economic calendar this week is free of major reports, except for the U.S. trade deficit in August. But preliminary data already revealed the trade gap widened sharply owing to a drop in exports. What’s more, the bulk of corporate profit reports for the third quarter won’t start arriving until the following week.

So investors, politicians and Fed bigwigs can chew over the September employment report for another week.

Some economists find the poor showing hard to swallow. Richard Moody, chief economist of Regions Financial, points to a rise in consumer spending, soaring auto sales, record-high job openings and a resurgent construction industry that’s benefited from a big uptick in home sales.

“That’s what is confusing,” he said. “They tell you a different story.”

Bernard Baumohl is even more skeptical. “Something is clearly amiss here,” said the chief economist of The Economic Outlook Group. He preaches a breath-deeply and wait-and-see approach.

A more pessimistic case can be drawn, however, from the struggles of energy producers and manufacturers.

Fueled by a domestic oil boom after the U.S. exited recession in 2009, American energy companies saw tremendous growth until the price of petroleum collapsed in mid-2014. Cheaper oil has forced big cutbacks, with the energy industry shedding 120,000 jobs since last December.

The loss of big-ticket orders for drilling rigs and the like was bad enough for U.S. manufacturers. But they have also been harmed by a soaring dollar that’s made American goods more expensive overseas, a problem compounded by a softer global economy. So exports have shriveled.

Although energy and manufacturing only account for a small percentage of all American jobs, these industries pay very well and that benefits the rest of the economy. Less jobs in those industries means fewer shoppers at retailers and fewer customers at restaurants, and so forth.

That’s why Wall Street will pay closer attention than usual to a normally secondary index that measures the health of the U.S. service sector, home to 80% of all American jobs. Economists polled by MarketWatch predict the ISM nonmanufacturing index will fall about 1.5 points in September from a very healthy 59.0 in August.

“A bigger drop would make investors nervous,” Moody said.

Washington, Oct 2, 2015 (AFP) A bleak September jobs report raised concerns about the US economy's resilience to the global slowdown and questions about the Federal Reserve's plan to lift interest rates this year. US job growth faltered in September and the labor market weakened across the board, the Labor Department said. The US economy added a disappointing 142,000 jobs in September, well below analyst estimates of 205,000. The already tepid August jobs level of 173,000 was revised sharply lower to 136,000, surprising analysts who had anticipated a large upward revision typical for that month. The July number also was lowered, bringing the average for the past three months to 167,000 jobs, lagging behind the 200,000-plus growth trend seen earlier in the year and in 2014. Just a month ago, the average had been 221,000, showing resilience to the turmoil triggered by China's shock currency devaluation in mid-August. "Two months of weak payroll gains suggest that the mighty US jobs machine may be losing some steam," said Nariman Behravesh, chief economist at IHS Global Insight. The downbeat labor picture came as the Federal Reserve considers its first interest rate hike since 2006. It suggested the economy was being hurt by the China-driven slowdown, which is dampening exports and manufacturing and roiling markets. The White House acknowledged the blow, noting "the economy added jobs in September at a pace below that seen earlier in the year, as slowing growth abroad and global financial turmoil have weighed on economic activity." The report also appeared to vindicate the September decision by the Federal Open Market Committee, the central bank's policy arm, to leave the benchmark federal funds rate near zero, where it has been pegged since 2008 to support the recovery from the Great Recession. "In retrospect, the decision by the Fed to hold fire seems like a good one. There has been a downshift in jobs growth and wage inflation remains very low. The earlier rationale for raising rates has now lost some validity," Behravesh said. The Fed has planned the liftoff for this year, and Fed chief Janet Yellen said as recently as last week that the timetable remained on track, but more improvement was needed in labor market conditions. The FOMC has two meetings left this year, in late October and mid-December, and there will be two more jobs report before year's end. Harm Bandholz, chief US economist at Unicredit, said the "employment report has most likely removed even the last small chance for a rate hike as early as this month." Patrick O'Hare at Briefing.com was more convinced. "One thing that seems certain in the wake of this report is that the Federal Open Market Committee won't be raising the target range for the federal funds rate at the October meeting -- not unless it wants to kill any and all credibility it has remaining," O'Hare said. - Dismal data - The jobs numbers were overwhelmingly bad, revealing weaknesses that the Fed views as signals of slack in the labor market. The unemployment rate, measuring those without work but actively seeking jobs, held unchanged as expected at 5.1 percent, the lowest level since 2008. The labor force participation rate, already extremely low, weakened further to 62.4 percent from the 62.6 percent of the prior three months. "Adding to the negative tone of today's report is the fact that the 0.2 percentage point drop in the participation rate to a 38-year low did not spur a further decline in the unemployment rate," Unicredit's Bandholz said. The number of unemployed people also was little changed at 7.9 million. Muted wage growth, an indicator of weak hiring demand, slowed. Average hourly earnings fell by one cent to $25.09, following a gain of nine cents in August. The year-over-year change in earnings was a modest 2.2 percent. The average workweek dropped by an hour. The stock markets, which had expected much stronger job growth, initially tumbled after the report but pared losses to turn positive around midday, ending in a strong rally, pushing the broad-market S&P 500 index up 1.4 percent. Tom Cahill, portfolio strategist at Ventura Wealth Management, said the jobs report made the outlook for the Fed rate hike "even more cloudy." "A lot of economists were looking at the September meeting to be the first interest-rate increase and then it was pushed out to December and now it's being pushed out to March," Cahill said.

1.a.tambahan :

New York, Sept 28, 2015 (AFP)

US stocks fell sharply Monday, joining European equities in retreat after poor Chinese industrial data deepened worries about the world's second-biggest economy.fokus UTAMA KRISIS 2015: Pertumbuhan Ekonomi CHINa

The Dow Jones Industrial Average fell 312.78 points (1.92 percent) to 16,001.89.

The broad-based S&P 500 lost 49.57 (2.57 percent) at 1,881.77, while the tech-rich Nasdaq Composite Index tumbled 142.53 (3.04 percent) to 4,543.97.

The losses put the S&P 500 back in correction territory, defined as a loss of 10 percent or more from its most recent high, in August.

Government data showed China's crucial industrial companies saw profits fall 8.8 percent in August from a year ago -- hit by last month's shock yuan devaluation, weak demand and plunging share prices.

The weak Chinese data hammered prices of key commodities such as oil and copper, as well as shares of petroleum-linked companies ConocoPhillips (-2.8 percent) and Schlumberger (-4.8 percent) and metals producer Freeport-McMoRan (-9.1 percent).

Art Hogan, chief market strategist at Wunderlich Securities, said investors are brooding over two key questions with no imminent resolution: when the Chinese economy will bottom out and when the US Federal Reserve will raise interest rates.

Adding to that are other worries, including potential legislation to rein in pharmaceutical prices and the Volkswagen emissions scandal.

"You have a path of least resistance that is lower until you have some answers to the big questions," Hogan said.

While the losses were broad-based, some sectors were especially bruised, including pharmaceuticals.

Valeant Pharmaceuticals International slumped 16.5 percent after Democratic lawmakers in Congress called for a subpoena for documents from the Canadian company allegedly related to related to huge drug price increases this year.

Bristol-Myers Squibb lost 4.6 percent, Dow member Pfizer dropped 3.4 percent and Gilead Sciences sank 5.3 percent.

Homebuilders also lost out after data from the National Association of Realtors showed US pending home sales fell in August. Lennar fell 5.7 percent, PulteGroup 4.7 percent and KB Home 8.0 percent.

Many technology stocks suffered drops, including Amazon (-3.7 percent), Facebook (-3.6 percent) and Netflix (-2.7 percent).

On the winning side was aluminum giant Alcoa, which jumped 5.7 percent on news it would split into two companies.

Also higher was Media General, which vaulted 22.3 percent on news it received an unsolicited buyout offer from Nexstar Broadcasting Group valued at about $4.1 billion. Nexstar dipped 2.3 percent.

Bond prices rose. The yield on the 10-year US Treasury fell to 2.10 percent from 2.17 percent Friday, while the 30-year dropped to 2.88 percent from 2.96 percent. Bond prices and yields move inversely.

Private firms tend to provide a better indicator of what's happening in the real economy

If you want to know where the economy is

heading, don’t look at the S&P 500. Look at what private companies

are doing. Over the last 20 years or so, both the number and size of

private firms in the US has grown. And—without the short-term pressure

of the public markets to contend with—they often provide a better window

into what is actually happening on Main Street rather than just Wall

Street. Look closely and you’ll find that private companies have

accurately predicted key issues such as where U.S. GDP growth is likely

to be in a year’s time and whether employment numbers will rise or fall.

So what is happening in private firms, and

what might it mean for interest rates (and consequently, the markets) as

the Fed considers a rate hike at its meeting this coming Wednesday and

Thursday? The consulting firm PwC came out Sept. 15 with its latest

Trendsetter data, a survey in which 300 private companies are asked how

their management feels about where the economy is heading, revenue

expectations, hiring intentions, investment focus, etc. The consensus

among these firms was that the U.S. is in a continued recovery, but not

one that’s gaining a tremendous amount of steam.

Hiring is up, but only by 2% or so–not enough

to create the kind of job market tailwind that would push wages up.

Firms expect that average hourly wages will only rise moderately

(roughly 3%) over the next year. Again, not the sort of uptick that

would boost growth in an economy made up 70% of consumer spending. Why

aren’t firms hiring more? The biggest impediment to hiring, according to

the surveyed firms, is lack of required skills in the jobs market. “The

private companies we survey want to hire more, but given the numbers of

long term unemployed in the US, there has been a lot of skill atrophy,

and firms either can’t find people with the skills they need, and aren’t

willing to offer big pay hikes to those they do hire given this,” says

PwC partner Ken Esch.

Combine still stagnant wage growth with low

commodities prices, and you don’t get much of an uptick in inflation.

That may well mean that the Fed could decide to keep the brakes on an

interest rate hike a bit longer. The question is, will more easy

monetary policy actually do anything to help Main Street? My sense is,

no, and it also delays the market correct that many people feel is

inevitable. But the Fed’s mandate is to keep employment high and

inflation low. With the former only just coming back to normal levels,

and the latter still lagging, the pressure will be on Fed Chair Janet

Yellen to keep rates low longer.

1b.

2.

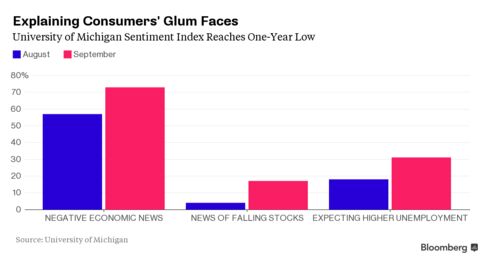

bloomberg: Consumer sentiment declined in September to the lowest level in a year as Americans anticipated a weaker economy in the face of a global slowdown and turbulent financial markets.

The University of Michigan’s preliminary index dropped to 85.7 from an August reading of 91.9, the largest one-month decline since the end of 2012. Households were less upbeat than a few months earlier about future growth in employment and wages, while 73 percent of respondents reported hearing of negative economic developments.

Some 17 percent of respondents mentioned unfavorable news about equity markets in September, the highest share since the height of the last financial crisis in October 2008. At the same time, sustained improvement in the labor market and cheaper gasoline will help shore up attitudes, which will garner the attention of U.S. central bankers as they consider raising interest rates as soon as next week.

“You’ve seen some fairly alarming news headlines over the last few weeks, and you would expect that to be reflected in consumers’ sentiment,” said Paul Ashworth, chief U.S. economist at Capital Economics NA Ltd. Still, expectations are “consistent with consumption growth of about 3 percent, which suggests a fairly healthy attitude toward buying.”

The median forecast in the Bloomberg survey of 67 economists called for a drop to 91.1. Forecasts ranged from 85 to 95.5. The 6.2 point monthly decline was the most since December 2012, when the government debated raising taxes and cutting spending to reduce the budget deficit.

Late August

While confidence dropped, the decrease in the first two weeks of September wasn’t as great as in the immediate aftermath of the plunge in stocks at the end of last month. The final August survey included an additional 64 consumers to gauge the reaction to market events, and the gauge for that group was 9.1 points lower than for those polled earlier.

“All in all, this is a very positive outlook,” Richard Curtin, director of the Michigan Survey of Consumers, said on a Bloomberg conference call. “Consumers have handled the news of the stock-market declines and its continued volatility quite well and they’re ready to put this behind them and continue on their spending path.”

Buying Plans

Attitudes in September toward purchases of automobiles and other big-ticket items remained strong, especially among higher-income households, the report showed.

The sentiment survey’s current conditions index, which measures Americans’ assessment of their personal finances, decreased to an 11-month low of 100.3 from a 105.1 reading in August. The measure of expectations six months from now fell to 76.4, the weakest in a year, from 83.4.

Americans projected an inflation rate of 2.9 percent in the next year, up from 2.8 percent in August. They thought prices to rise 2.8 percent over the next five to 10 years, compared with 2.7 percent the previous month.

“While the current strength in consumer spending is still likely to persist, the more lasting impact of recent events may be a heightened attentiveness to potential negative developments,” Curtin said in a statement.

Fed Meeting

He held out the possibility that households would view an interest-rate increase next week by the Federal Reserve as adding to recent negative developments in global capital markets.

“If economic growth proceeds as widely anticipated, the small delay of a rate hike to October or December will not matter,” Curtin said. “A September rate hike, however, may add some unnecessary risks to an otherwise positive outlook.”

Another sentiment measure reflected the impact of the recent market correction. The Bloomberg Consumer Comfort index stalled last week as weaker perceptions about the buying climate offset more sanguine views of household balance sheets.

With the turmoil in global markets, consumers will need to see continued strength in employment in order to stay positive on the economy. They may take some comfort in the August payrolls figures, which showed the jobless rate fell to a seven-year low and is now in the range that Fed officials consider full employment.

Meanwhile average hourly pay increased 2.2 percent last month from a year earlier, tracking within the same lackluster band that’s characterized the entire expansion since mid-2009. Fed officials will consider the jobs data as they debate whether the economy and financial markets are strong enough to withstand higher interest rates.

Disposable Income

Falling energy prices should give households more disposable income to spend some place other than the gas station, offering relief from the stagnant wages. The average price of a regular gallon of gasoline fell to $2.37 on Sept. 9, the lowest level since Feb. 25.

Stabilization in the stock market may also help buoy confidence among the households that hold such assets. Market instability as measured by the Chicago Board Options Exchange Volatility Index has moderated but remains elevated since China devalued the yuan on Aug. 11.

The S&P 500 index lost 6.3 percent in August, the worst month for the stocks gauge since May 2012. So far for September, it’s down 1 percent through Thursday.

That has companies such as Williams-Sonoma Inc. keeping an eye on how the turbulence might affect their business.

“It goes without saying that a significant and sustained pullback in the stock market could lead to a reduction in consumer confidence and impact the discretionary spending landscape,” Chief Executive Officer Laura Alber said on an Aug. 26 conference call, adding that she was still confident in the company’s ability to gain market share. “We’re watching the markets along with everyone else.”

3.

Bisnis.com, JAKARTA--Spekulasi penaikan suku bunga The Fed seusai rapat Federal Open Market Committee (FOMC) pada Kamis (17/9), tidak hanya menjadi kekhawatiran Indonesia, tetapi juga banyak negara lain.

Plt Kepala Eksekutif Lembaga Penjamin Simpanan (LPS) Fauzi Ichsan mengatakan spekulasi penaikan Fed Rate menjadi kekhawatiran pelaku pasar global. Namun, ia melihat ada potensi The Fed menunda penaikan suku bunga.

"Bukan kekhawatiran spesifik pelaku pasar Indonesia, tetapi banyak negara yang mengkhawatirkan prospek kenaikan suku bunga AS," kata Fauzi di Kompleks Istana Kepresidenan, Rabu (16/9/2015).

Melihat perkembangan perekonomian AS, Fauzi justru melihat potensi penundaan penaikan suku bunga The Fed semakin besar.

Alasannya, antara lain dolar AS telah menguat sangat tajam, tingkat inflasi rendah, dan jumlah penduduk setengah menganggur masih besar. Selain itu, seiring melorotnya harga komoditas energi, ekspor AS tertekan.

Apalagi, lanjutnya, bank sentral negara lain, seperti Jepang, Tiongkok, dan Uni Eropa justru menerapkan kebijakan moneter ekstra longgar. Tidak hanya memangkas suku bunga, tetapi juga menggulirkan quantitative easing.

"Bisa ditunda sampai semester I/2016," imbuhnya.

Sementara itu, Ketua Dewan Komisioner Otoritas Jasa Keuangan Muliaman D. Hadad enggan mengomentari spekulasi penaikan Fed Rate seusai rapat FMOC pada Kamis (17/9).

"Kita tunggulah. Saya enggak mau terlalu cepat juga mengomentari. Mudah-mudahan nanti tidak apa-apa," kata Muliaman.

4.

marketwatch: Former Treasury Secretary Lawrence Summers seems to have invited himself to the Federal Reserve’s September meeting.

Summers’ latest bog post is written like he’s pulled up a chair at the Sept. 16-17 Fed policy committee gathering and is warning his colleagues against a rash rate hike.

Economists think a rate decision at the September meeting is a close call.

Summers was at one point close to joining the Fed. He was, by all accounts, President Barack Obama’s choice to replace Ben Bernanke as Fed chairman. But Obama ultimately chose to reappoint Bernanke in 2009 and then picked Janet Yellen over Summers four years later after a revolt of liberal Senate Democrats.

Neil Dutta, head of U.S. economics for Renaissance Macro Research, said Summers has been reinventing himself as the “working man’s economist” ever since Senate Democrats torpedoed his Fed nomination.

Summers does make a forceful dovish case for the Fed to stand pat, warning that, if some of the global fears surrounding China and a global slowdown ultimately prove warranted, a tip of the Fed toward tightening “risks catastrophic error.”

In contrast, Yellen seems somewhat more hawkish, having expressing a desire to hike rates at some point this year. But, to be fair, the Fed Chairwoman’s current stance on rate policy is unknown. She has not spoken publicly since China’s surprise devaluation in mid-August, which set off the current round of global financial market turmoil and threw a September rate hike into doubt.

In his blog post, Summers made five points against a September rate hike.

Data suggest slowing in the U.S. and global economies.

Market-based inflation expectations suggest core inflation will remain well below 2%

Arguments for “one and done” are “specious,” with the case for hitting the brakes even once not there.

Conventional wisdom China is in its most uncertain state since it began economic reform in 1979

Markets have already done the work of tightening, as financial conditions as measured by Goldman Sachs or the Chicago Fed index already tighter by more than a 25 basis point tightening.

5.

BANDUNG, KOMPAS.com - Pelaksana Tugas (Plt) Kepala Grup Pengelolaan Relasi Bank Indonesia (BI), Arbonas Hutabarat mengatakan, ketidakpastian Bank Sentral Amerika Serikat (AS) Federal Reserve menaikkan suku bunga acuannya telah membuat banyak orang mengambil ancang-ancang. "Bagi BI, lebih cepat The Fed menaikkan suku bunga lebih baik karena kita bisa menghitung keseimbangan baru," kata Arbonas di Bandung, Sabtu (5/9/2015).

Dia lebih lanjut bilang, jika ada kepastian level suku bunga acuan baru, BI bisa segera mengetahui penyesuian kebijakan apa yang mesti dilakukan. Membaiknya perekonomian negeri Abang Sam, menurut Arbonas telah membuka ruang bagi The Fed untuk menaikkan suku bunganya. "Sejak Mei 2013 sudah diumumkan, di sinilah mulai ketidakpastian pasar," kata dia.

Ketidakpastian pasar terjadi lantaran kenaikan suku bunga The Fed diyakini bakal menggiring dana masuk ke AS. "Teori finance natural orang akan mulai melirik AS," imbuh dia.

Indonesia pun tak lepas dari gejolak ketidakpastian ini. Sebab dana-dana asing yang ada di Indonesia cukup banyak seperti 36 persen di pasar obligasi dan 60 persen di pasar modal. Kendati begitu, menurut Arbonas, tidak semua dana asing di emerging markets seperti Indonesia akan pulang kampung ke AS. "Akan ada rebalancing portfolio asing sesuai dengan keyakinan risiko atas fundamental sebuah negara," ucap Arbonas meyakinkan fundamental RI masih cukup baik.

Penulis

: Estu Suryowati

Editor

: Josephus Primus

6.

investing.com:

October Rumors

Amidst the tumultuous run in equities over the last week, traders pared expectations of a September liftoff for the Federal Reserve as weak inflation coupled with worsening external financial conditions led to a rise in expectations that the FOMC would be forced to delay any policy adjustments. However, rumors are now swirling that October could prove the next date to watch, especially if inflation is able to start trending towards the levels targeted by the Central Bank’s mandate. Evidence of this comes amid a rebound in the US dollar after data released today showed that US durable goods orders rose more than forecast with thecore number rising 0.60% and the regular figure up 2.00% month over month. Certain Federal Reserve voting members including Atlanta President Dennis Lockhart are sticking to the narrative that expects interest rates to rise this year. Analysts have attributed recent market volatility to investors preparing for the possibility that September will be the first hike in 9 years, contributing to the pace of exits from risky positions.

In another instance of the tail wagging the dog, markets are reducing forecasts for a September hike, hoping that the recent bout of volatility will be warning enough to Federal Reserve to prevent liftoff. To a degree, volatility was anticipated ahead of September due to the expectation that rising rates would create a selloff in equity markets while forcing a rebalancing in foreign-exchange markets as the stronger US dollar would force other countries to abandon their pegs. Currencies such as theSaudi Arabian Riyal and Hong Kong dollar, which are currently exchanged at a fixed rate to US dollars might be forced to move to free float as the dollar strength saps competitiveness from these economies. The volatility witnessed earlier in the week could be attributed to China, with its own problems seemingly at the epicenter of recent losses. However, in conjunction with possible risk-off moves being made by the smart money, the sheer scale of the momentum could be indicative that other forces were at play as investors and speculators reposition ahead of what could be policy normalization in coming months despite reduced forecasts for a September hike.

marketwatch

New York Fed President

William Dudley, a pivotal member of Fed Chairwoman Janet Yellen’s inner

circle, backed away Wednesday from supporting an interest-rate hike at

the U.S. central bank’s September meeting.

Wild swings in global

financial markets, the slowing Chinese economy and falling commodity

prices have increased the “downside risks” to the U.S. economic outlook

somewhat, Dudley said in brief remarks to reporters Wednesday.

There

could be less demand for U.S. goods and services, as strains are rising

on emerging economies, he said. And the drop in stock prices

effectively has had the same impact as higher interest rates by

tightening financial market conditions.

“The bottom line: we have

been assessing domestic and international financial markets closely in

terms of their implications for the U.S. economic outlook and we will

continue to do so. From my perspective, at this moment, the decision to

begin the normalization process at the September FOMC meeting seems less

compelling to me than it was a few weeks ago,” Dudley said.

The New York Fed President is a fairly dovish U.S. central banker. But more important, he is seen as reflecting Yellen’s views.

Dudley

said it was important not to overreact to the stock-market tumble and

stressed his views could change again before the Fed meeting on Sept.

16-17.

Recent economic data has been “pretty positive” lately,

including the “good increase” August consumer confidence data, “solid”

July new home sales and today’s durable goods report, he said. But the

Fed also has to take into account the troubling international

developments.

“At the end of the day, we’re concerned about the outlook,” he said.

“The stock market really has to move a lot and stay there for it to have implications for the U.S. economy,” he said.

8.

bloomberg: U.S. stocks erased most of a selloff sparked by a worsening rout in emerging markets and a plunge in oil as Federal Reserve minutes showed policy makers judged conditions for higher rates haven’t been met yet.

The Standard & Poor’s 500 Index fell 0.2 percent to 2,093.85 at 2:16 p.m. in New York, after dropping as much as 1.3 percent earlier.

“Almost all voters needed more evidence on inflation,” said Anthony Valeri, a market strategist with LPL Financial Corp. in San Diego. “Since the meeting, inflation expectations have declined, the dollar has increased further and China has devalued its currency. That would argue against a Fed rate hike.”

Fed officials said last month that while conditions for raising interest rates were approaching, they saw more room for labor market healing and need more confidence that inflation is moving toward their goal, minutes of their meeting show.

The Fed gathering preceded China’s surprise devaluation on Aug. 11 that prompted some investors to scale back bets on a rate increase in September. Those odds were reduced further on Wednesday, with traders pricing in a 40 percent probability of a rate move next month.

The selloff gripping emerging markets isn’t letting up as stocks drop to four-year lows and countries including Vietnam and Kazakhstan weaken their currencies to adjust to the fallout from China’s shock devaluation last week. Meanwhile, oil has tumbled more than 30 percent since this year’s peak amid signs that producers are maintaining output despite surpluses.

U.S. stocks slumped earlier in the day with global equities, with the S&P 500 falling below its average price for the past 200 days, as the Stoxx Europe 600 Index tumbled 1.8 percent.

9.

Bisnis.com, JAKARTA- Bank sental Amerika Serikat Federal Reserve akan merilis hasil pertemuan Juli pada Rabu (19/8/2015).

Pedagang telah meningkatkan harapan adanya kenaikan Fed Rate pada September, yaitu dengan probabilitas naik menjadi 46 % dari 40% pada Selasa, menurut data perdagangan berjangka yang dikumpulkan oleh Bloomberg.

"Saya suka pasar ekuitas AS di sini," Adam Parker, Kepala Strategi Ekuitas AS Morgan Stanley, seperti dikutip Bloomberg, Selasa (18/8/2015).

Namun tidak sedikit yang menyoroti tanda-tanda pertumbuhan Eropa, dan harapan bahwa Federal Reserve tidak segera menaikkan suku bunga.

"Saya tidak berpikir ada alasan untuk repot-repot dengan itu. Gagasan itu akan menjadi sangat lambat dan menunggu enam bulan lagi," kata Daniel Brehon, Ahli Strategi Deutsche Bank AG seperti dikutip Bloomberg, Selasa (18/8/2015).

10.

marketwatch: So much for that “one-time correction.” The People’s Bank of China let

the yuan drop again overnight, fixing the currency 1.6% below Tuesday’s

close, following the 1.9% devaluation heard around the world a day ago.

Cue continued freakout for global markets.

Deutsche

Bank, for one, is predicting the yuan is overvalued by around 10%, so

if the yuan continues to weaken, things could yet get a lot darker for

markets. And stocks aren’t dealing well with the new China reality

they’ve seen so far. Jani Ziedins of the Cracked Market blog

says the U.S. market’s reaction — the S&P 500 fell 1% Tuesday, and

futures are pointing sharply lower on Wednesday — looks a bit overdone.

Still, he says, it’s understandable given the reasons behind it — fears

of much bigger economic problems in China. Good news? “...if a crumbling

Chinese economy cannot bring down this market, then nothing will and

all we can do is hang on and enjoy the ride,” he says.

Ziedins

says watch the next two days to get some insight into the market’s

psyche. Either selling is revving up to drop this market to levels not

seen in years or this emotional purge will exhaust itself, and a rebound

will follow, he predicts. Our chart of the day shows just how long it’s

been since the S&P 500 has had a decent correction.

But if death crosses and visions of rotting Apples

are disturbing your sleep, you aren’t alone. ”The darkest horizon ever

approaches, infused with Chinese black coal,” predicts the Fly, blogging

for iBank Coin. It’s time to be cautious, he says. More on that here.

If

you really want to shiver your timbers, then check out our call of the

day. One of the biggest bears out there is riding the China devaluation

to the hilt, talking boils and puss and predicting a financial crisis a

la 2008. Brr...

Key market gauges

Wall Street is set to get beat up again, with futures for the S&P 500

ESU5, -0.71%

and Dow

YMU5, -0.74%

down 0.7%. In Asia, emerging currencies got knocked around, the Hang Seng

HSI, -2.38%

dropped 2%, and Australian stocks

XAO, -1.64%

and the Nikkei

NIK, -1.58%

fell by around 1.6% each. The dollar

USDJPY, -0.75%

hit a two-month high against the yen. European stocks

SXXP, -2.09%

are also getting slapped around.

Elsewhere, gold

GCZ5, +0.68%

is up and crude oil

CLU5, +0.60%

is rallying after an

International Energy Agency report on the state of supply and demand.

The stat

Oil demand is growing at its fastest pace in five years, says the International Energy Agency. That’s the good news. The bad news? Rival production will only start to taper off next year.

The quote

“If

we turn around and nix the deal and then tell them, ‘You’re going to

have to obey our rules and sanctions anyway,’ that is a recipe, very

quickly ... for the American dollar to cease to be the reserve currency

of the world.” — U.S. Secretary of State John Kerry speaking about Iran

at a Reuters Newsmaker event on Tuesday.

Earnings

China’s top e-commerce provider AlibabaBABA, -4.90%

is getting dinged in premarket after revenue fell short of estimates. Macy’sM, +0.22%M, +0.22%

is coming up.

After the close, CiscoCSCO, -1.99%

and News Corp. (the publisher of MarketWatch) will report. More on moving stocks here.

The economy

New

York Fed President William Dudley will speak on the economic outlook in

Rochester NY at 8:30 a.m. He’s known to be one of the most dovish

members of the FOMC. Watch any Q&A and comments on China, as well as

clues about a September hike.

A report on job openings comes at 10 a.m.

Investing.com - The dollar turned lower against the other major currencies on Tuesday, after data showed that U.S. unit labor costs rose more than expected in the second quarter, while non-farm productivity came in below forecasts.

The U.S. Bureau of Labor Statistics reported on Tuesday that unit labor costs increased by0.5% in the three months to June, above forecasts for a gain of 0.1% and following rise of 2.3% in the first quarter.

The report also said that nonfarm business sector labor productivity increased by 1.3% in the second quarter, missing expectations for a gain of 1.6%. The previous quarter’s figure was revised to a drop of 1.1% from a previously reported fall of 3.1%.

The dollar has strengthened earlier in the day, after China devalued the yuan in an attempt to help exporters after a recent spate of disappointing economic data.

The central bank described it as a “one-off depreciation” of nearly 2%, based on a new way of managing the exchange rate that better reflected market forces.

EUR/USD gained 0.37% to 1.1062. The ZEW Centre for Economic Research earlier said that its index of German economic sentiment fell by 4.7 points to a nine-month low of 25.0 this month from July’s reading of 29.7.

Analysts had expected the index to rise by 2.3 points to 32.0 in August.

Separately, a Greek official said early Tuesday that his government had completed talks with creditors over a deal setting out the terms of a third bailout, with some details remaining.

Elsewhere, the dollar was steady against the pound, with GBP/USD at 1.5589 and lower against the Swiss franc, with USD/CHF down 0.13% at 0.9824.

The Australian and New Zealand dollars were still sharply lower, with AUD/USD down 1.20% to one-week lows of 0.7322 and with NZD/USD tumbling 1% to 0.6551.

Earlier Tuesday, the National Australia Bank reported that its business confidence indexfell to 4 in July from a reading of 8 in June, whose figure was downwardly revised from a previously estimated reading of 10.

Analysts had expected the index to rise to 11 last month.

Meanwhile, USD/CAD climbed 0.58% to trade at 1.3078.

The U.S. dollar index, which measures the greenback’s strength against a trade-weighted basket of six major currencies, was down 0.18% at 97.05.

12.

Pulling most investors out of the summer lull, China’s central bank

early Tuesday surprised global markets by devaluing its tightly

controlled currency, triggering the largest one-day loss for the yuan in

two decades.

The dollar

USDCNY, +1.8550%

jumped to buy 6.3294 yuan.

That’s up from around 6.2058, the range where it’s been trading in

recent months, mainly due to Beijing’s intervention

dollar-yuan

The People’s Bank of China allowed the yuan

to devalue by 1.9%, in an effort to boost flagging exports and spur

growth in the world’s second-largest economy. It also allows the

currency to be driven more by market forces.

While

the central bank stressed the move was a one-off depreciation, analysts

are concerned it could be the opening salvo in a new currency war — and

that it might affect the prospects for a September rate rise from the

Federal Reserve.

Here are some of the initial assessments of the devaluation from analysts:

“It’s quite likely that the larger-than-expected fall in exports in July

that was announced over the weekend had something to do with the move.

I’ve been saying for some time now that the slowdown in global trade,

plus the deflationary pressures from falling commodity prices (which

themselves may be just a symptom of falling demand, too) would be likely

to restart the ‘currency wars.’ Now we have the first shot fired.

Although China said this was a one-off move, other countries are likely

to be wary. Who will be first to react?”

“I doubt if it will

derail the Fed’s plans to tighten, but it may well slow the pace of

their tightening. It could have a bigger impact on the actions of the

Bank of England, where the mandate is focused entirely on inflation. ” —

Marshall Gittler, head of global FX strategy at IronFX

“What

is of interest is how the U.S. will react to this move. It will almost

certainly cause [Fed Chairwoman] Janet Yellen and the Fed more problems

and could possibly kill off the September rate hike, as any further

gains by the U.S. dollar could cause more problems for the U.S.

economy... . It is clear that the ‘currency war’ is back, which will

make the next few weeks very interesting.” — Nour Al-Hammoury, chief market strategist at ADS Securities

“We

believe this new mechanism, if followed through, marks a revolutionary

move towards improving the CNY exchange rate formation mechanism...

While the PBoC will likely still not wholly transfer determination of

the currency to the market, it is a major step in that direction.

However, if there are sharp moves on a day-to-day basis, we would expect

the authorities to step in and prevent sharp moves in the fixing, even

if the market was implying a bigger move.” — Analysts at Barclays

“This

was a shock to otherwise sleepy summer markets, and follows several

weeks of inactivity on this front, where the spot and daily fix have

barely moved for months. The markets were looking for [reserve

requirement ratio] cuts, not this revaluation/depreciation... By

surprising the market today, at least the PBoC has mitigated the

potential for capital flight.” — Annette Beacher, chief Asia-Pacific macro strategist at TD Securities

“Coming

on the back of yet another set of poor export readings, the timing of

the move is certainly not ‘happenstance’ and per se raises the suspicion

that this was far from a ‘one-off’ move... Let us also not forget that

China’s Real Effective Exchange Rate (REER), as calculated by the [Bank

for International Settlements], has risen by some 14% in the past year,

today’s 2% drop pales into insignificance. Of course, markets that are

already fretting about Fed rate lift-off will not appreciate this

surprise, but in truth, this has been coming for quite some time.” — Marc Ostwald, FX strategist at ADM Investor Services

“How

important is this? For China, it matters a lot. For global currency

markets, it is a major change. But for the global economy, the impact

should be pretty small... All in all, this may be a step for China to

make its currency a little more flexible, and manage it more relative to

a genuine basket of other currencies, rather than mostly relative to

the U.S. dollar. It introduces an additional element of volatility into

global FX markets. However, this adjustment does not affect the outlook

for, say, European exporters to China very much.” — Holger Schmieding, chief economist at Berenberg

13.

New York, Aug 10, 2015 (AFP) The dollar fell against the euro Monday as Federal Reserve officials' comments raised questions about the timing of the central bank's plan to raise its key interest rate this year.

After last Friday's solid US jobs report for July, many analysts saw support for the Fed to raise its zero-level benchmark federal funds rate in September. Others said the Fed would probably wait until later in the year, or even until 2016, to make the first lift-off since May 2006.

"Gains for the dollar have proven tougher to hold on to these days, a reflection of the still uncertain climate for Fed policy and how higher borrowing rates have largely been baked into its value," said Joe Manimbo, senior market analyst at Western Union Business Solutions.

The Fed began the tightening cycle in September 2007, finally bringing the fed funds rate to essentially zero in late 2008 to help support the economy's recovery from the Great Recession.

While the job market has improved to near full-employment levels, inflation has remained tepid, well below the Fed's 2.0 percent target, and the economy has achieved only a slow recovery, making the decision to tighten credit without derailing growth a tough call.

Fed Vice Chairman Stanley Fischer said Monday that low inflation remains a concern, although the Fed thinks it is due to transitory factors such as lower oil prices.

"Employment has been rising pretty fast relative to previous performance, and yet inflation is very low," Fischer told Bloomberg Television. "And the concern about this situation is not to move before we see inflation, as well as employment, returning to more normal levels."

Atlanta Fed President Dennis Lockhart appeared to raise the prospect for a hike sooner rather than later.

"We are getting closer and closer to what feels like a healed state of the economy," Lockhart said in prepared remarks to the Atlanta Press Club.

"I think the point of liftoff is close." <pre> 2100 GMT Monday Friday EUR/USD 1.1019 1.0962 EUR/JPY 137.31 136.16 EUR/CHF 1.0839 1.0786 EUR/GBP 0.7068 0.7076 USD/JPY 124.72 124.22 USD/CHF 0.9837 0.9840 GBP/USD 1.5590 1.5492 </pre>

14.

Bisnis.com, JAKARTA - Bank Indonesia menyatakan pelemahan nilai tukar rupiah sepanjang tahun ini berbeda dengan tahun sebelumnya.